Governor Adriana D. Kugler

Thank you for the opportunity to speak here at the ECB today.1 I am particularly pleased to be part of this year’s conference because the theme you have chosen has, for some time now, also been a theme of my career as an academic and public servant. Every day, of course, central bankers must bridge science and practice, drawing on the insights that research provides, specifically, because the economy and the world are continuously subject to new circumstances. We must do so, and put those insights into practice, because everyone in the United States, and in Europe, and around the world, depends on a healthy and growing economy, and depends on policymakers making the right decisions to help keep it that way.

But well before I came to the Federal Reserve, I was also bridging science and practice. First, as a labor economist, when, for example, I was exploring how employment, productivity, and earnings are influenced not only by educational attainment and experience, but also by policies. Later, as chief economist at the Department of Labor, I brought science to bear in carrying out its mission of supporting workers. As the U.S. representative at the World Bank, economic science was likewise crucial in deciding how to best direct the institution’s resources to where they were needed the most. In each of these roles, I have learned a bit more about the need to balance rigorous scientific understanding of the problems that people face with the real-world experiences of those people, which sometimes do not fit so neatly into an economic theorem or principle.

Most recently, my colleagues and I on the Federal Open Market Committee (FOMC) have been focused on the very practical task of reducing inflation while keeping employment at its maximum level. To understand the recent experience of high inflation in the United States, it is helpful to consider how inflation behaved around the world after the advent of the COVID-19 pandemic. In the remainder of my remarks, I will discuss the global dimensions of the recent bout of high inflation in different economies, both comparing similarities and contrasting differences, with a special emphasis on the factors that enabled the United States to achieve disinflation while having stronger economic activity relative to its peers. I will then conclude with some comments on the U.S. economic outlook and the implications for monetary policy.

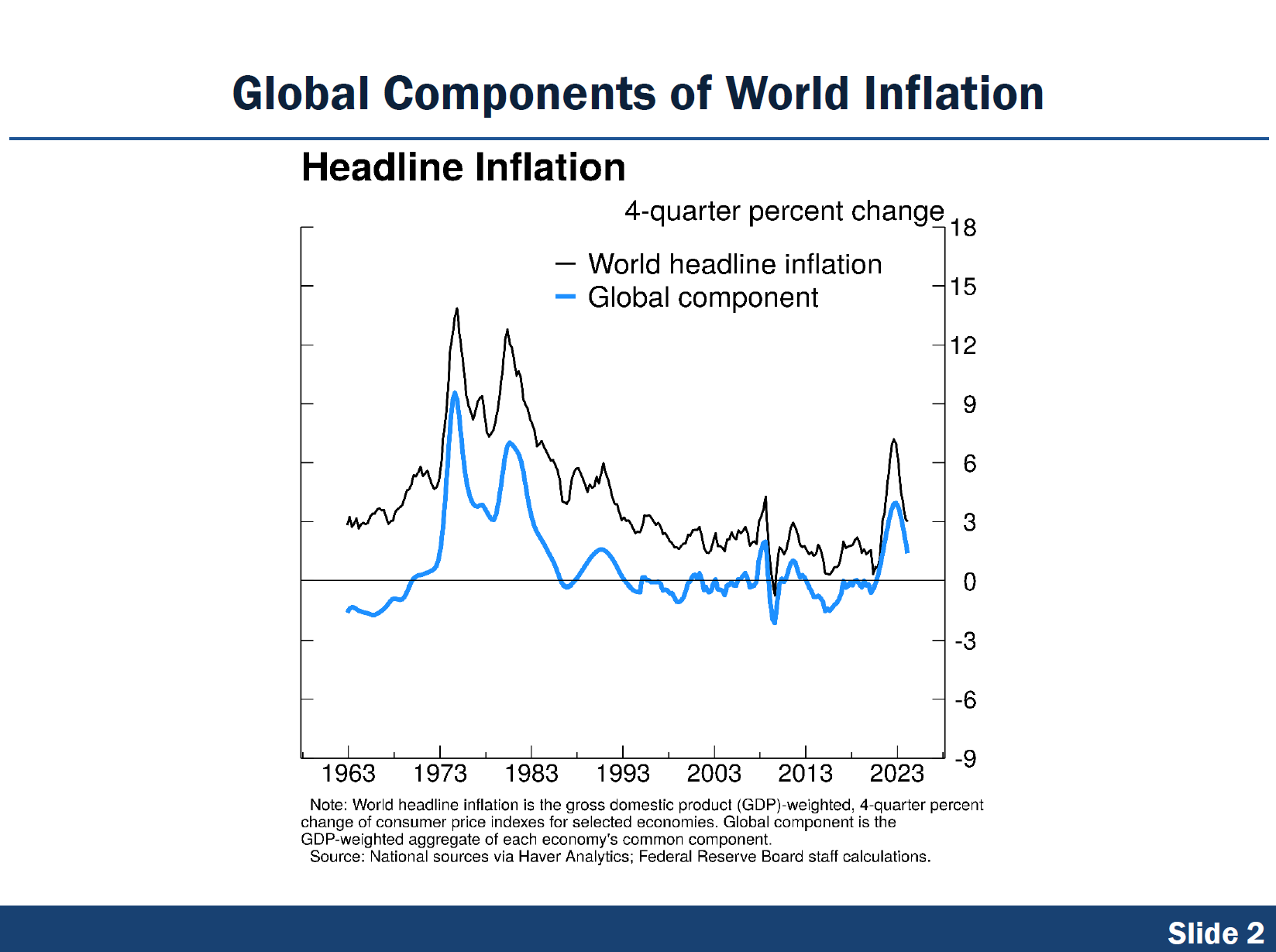

Starting with the similarities in our inflationary experiences, in early 2020, a worldwide pandemic disrupted the global economy and ultimately caused a surge of inflation around the world. Global goods production was hobbled, transportation and other aspects of supply chains became entangled, and there were significant labor shortages, all combining to cause a severe imbalance between supply and demand in much of the world. Sharp increases in commodity prices were exacerbated by Russia’s invasion of Ukraine. The result was a global escalation of inflation. As you can see by the black line on slide 2, a measure of world headline inflation in 26 economies accounting for 60 percent of global gross domestic product (GDP) rose to a degree that had not been experienced since the early 1980s.

This worldwide increase of inflation was synchronized and widespread across advanced and emerging economies. To measure the synchronization and breadth of this inflationary period, Federal Reserve Board researchers have employed a dynamic factor model to estimate a common component of inflation across these 26 economies.2 As you can see by the blue line on slide 2, the estimated global component accounts for a large share of the variation of headline inflation among these economies after inflation began rising sharply in 2021. This evidence is consistent with the familiar story of widespread lockdowns, shutdowns of manufacturing plants in different parts of the world, disrupted logistic networks, increases in shipping costs, and longer delivery times. In the recovery, we also saw globally higher demand for commodities, intermediate inputs, and final goods and services, with demand exceeding a still-constrained supply.

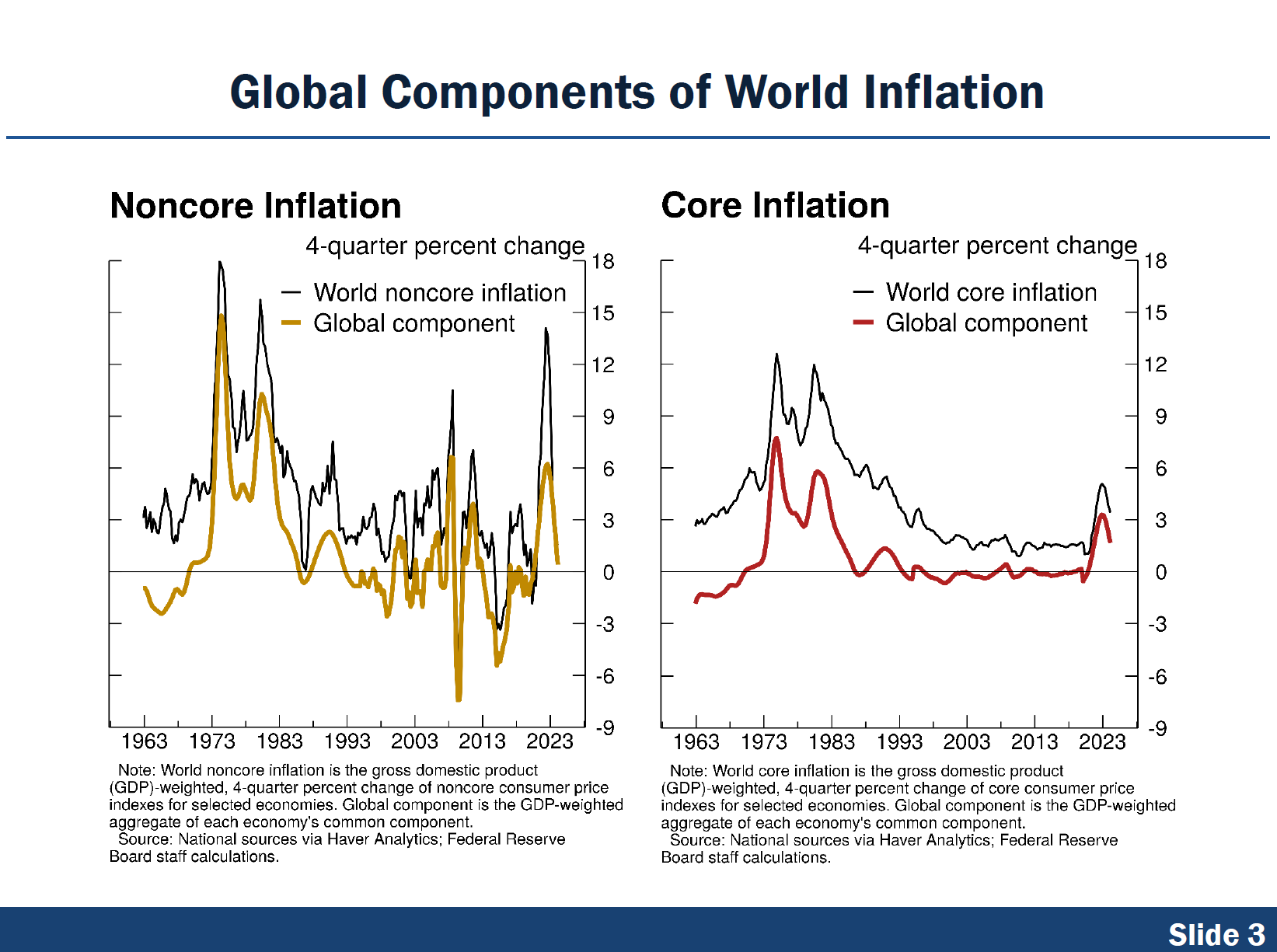

Indeed, one important contributor to the recent co-movement in inflation across the world has been food and energy prices. As you know, most of the time variations in inflation are heavily influenced by food and energy prices, which tend to be more volatile than the prices for other goods and services. Because many food and energy commodities are traded internationally, retail prices paid by consumers also tend to have some degree of global synchronization. Thus, as you would expect, the black line in the left chart on slide 3 shows that food and energy inflation faced by consumers around the world—here called noncore inflation—rose substantially in the recent inflationary episode. Moreover, world noncore inflation is largely accounted for by its global component in yellow, thus also showing a high degree of global synchronization.

Another thing we can say about the recent worldwide escalation of inflation is how widely diffused it was across different price categories. Core inflation excludes food and energy prices, and it includes many categories more exposed to domestic conditions such as housing and medical services. Yet, as shown by the black and red lines in the right chart on slide 3, the recent rise in core inflation showed a high degree of global synchronization, with the global component accounting for a large share of the post-pandemic inflation. Looking back in history, this is the first time since the 1970s that we saw a rise in core inflation so widespread across such a large number of countries. Moreover, underlying this rise in core inflation in the United States and other advanced economies, research carried out by Federal Reserve Board economists shows that there was a widespread rise in prices across the whole range of categories within the core basket.3

Academics and policymakers have debated about the possible reasons explaining the recent co-movement of inflation around the world. The COVID-19 pandemic was a global phenomenon and had effects on supply and demand that were similar in many countries. On the supply side, businesses closed, affecting goods production and the provision of services. There were labor shortages due to illness, social distancing, early retirements, and declines in immigration, with all of these factors making it harder to produce goods and services.4 Production disruptions and labor shortages propagated around the world due to long and intricate supply chains forged over several decades of growing globalization in trade. The imbalance between supply and demand widened as consumers switched their spending from services to goods, straining transportation capacity that further disrupted supply chains.5 This re-allocation of demand from services to goods also strained the ability of firms to produce, as they struggled to find qualified workers due to the needed re-allocation of workers across sectors.6 This demand was also likely fueled by the fiscal response to COVID-19 in 2020 and 2021. All of these factors drove up costs, and there were others. Russia’s war on Ukraine intensified the increases in energy and food commodity prices during the recovery from the pandemic. And the interaction of these different forces also likely played a role.7 For example, as Asia increased production to meet higher demand for goods in the U.S., this may have driven up wages and other input costs in Asia, increasing demand for imports from other places and, in turn, raising costs there, and so on. My assessment is that both supply and demand contributed to the recent global inflationary episode, including in the United States, with international trade of goods, including commodities, and services playing an important role in disseminating these forces around the world.

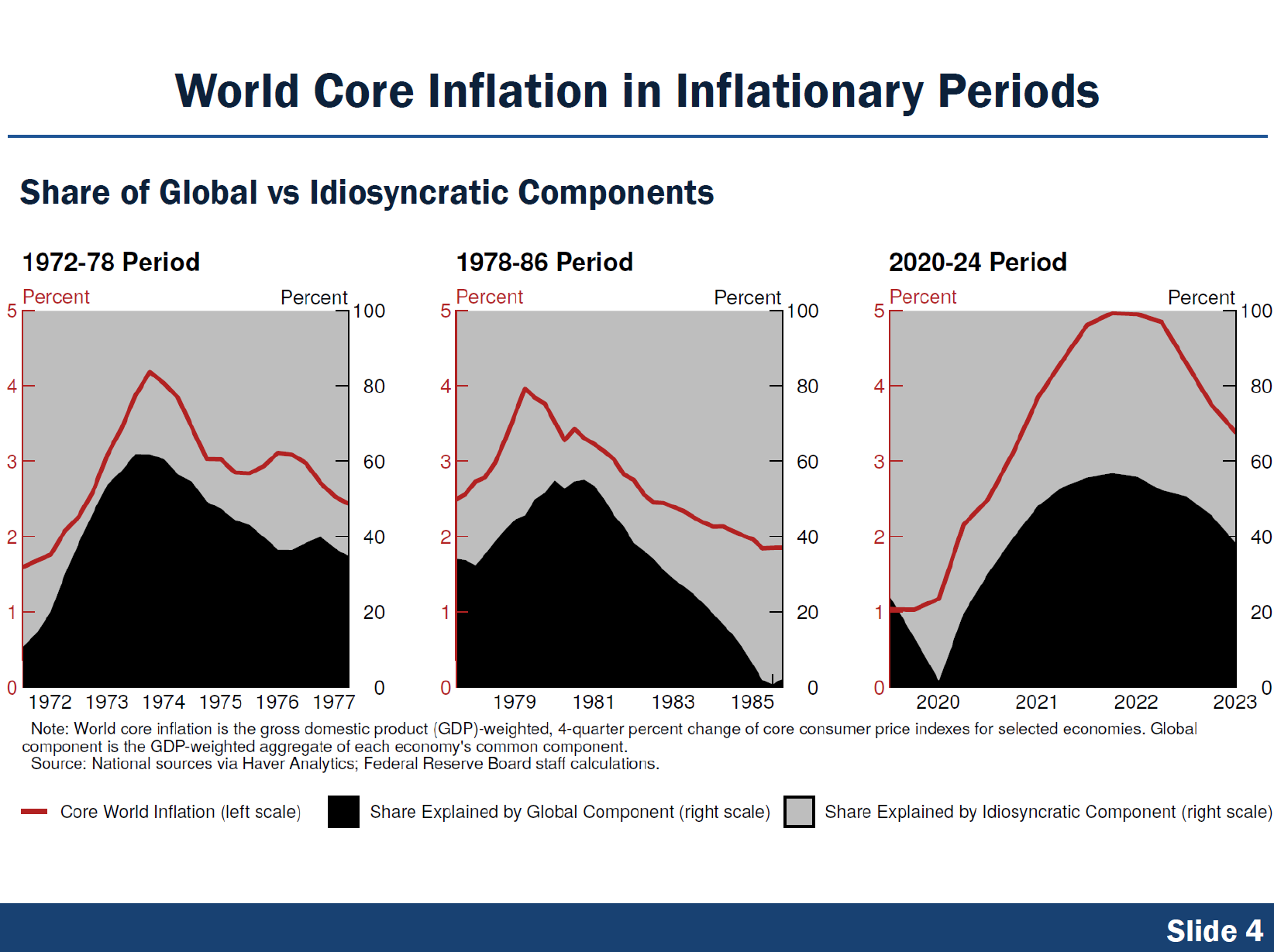

One salient aspect of past inflationary episodes is the observation that core inflation typically falls more slowly than it increases. As we can see by the red lines on slide 4, world core inflation rose more quickly than it decreased in the three most recent episodes of significant inflation and disinflation—from a trough in 1972 to a new trough in 1978; from 1978 to a trough in 1986; and then the recent episode, from the end of 2020 through the first quarter of 2024. In these episodes, the escalation of four-quarter core inflation increased by an average of 7/10 percentage point per quarter to its peak, while it decreased by an average of only 3/10 percentage point per quarter to the trough.8

Still, it is important that central bankers not only compare similarities across economies in the recent inflation fight, but also contrast the differences. Notably, another important feature of the last three inflation and disinflation periods is that though the share of core inflation explained by the common component increases when inflation rises, this share decreases when inflation falls, as can be seen by the black shaded areas of the three panels on slide 4. This suggests that while the reasons underlying the co-movement of inflation across the world—such as global supply disruptions and commodity price shocks—may have been important when prices were increasing, they have been less important when prices have decreased. This evidence indicates that factors that vary from economy to economy become more relevant in the disinflationary period.

Economic researchers have raised several possible explanations for the different inflation trajectories experienced by different economies during this post-pandemic period. For example, some point to differences in the magnitudes of the demand and supply imbalances driven by the shutdown and reopening of each economy, with this imbalance possibly playing a larger role on inflation in the euro area relative to the United States.9 While noting that differences in the size of fiscal stimulus in different countries were likely important, the targeting of that stimulus also differed, in some cases with a greater emphasis on addressing supply disruptions.10 Global factors also affect various economies differently, with studies showing that the exposures to fluctuations in commodity prices are an important issue.11 For instance, Europe was heavily affected by natural gas shortages related to Russia’s war on Ukraine, while gas supplies in the United States were more plentiful during this period. Also, supply chains were untangled at different speeds in different parts of the world, with, for instance, low water levels in the Panama Canal and attacks in the Red Sea by Houthi rebels affecting different shipping routes differently around the world. And, last but not least, differences in labor market tightness very likely played a role, with evidence pointing to its importance in the United States in driving up nominal wage growth, a factor that likely helped keep employment and economic activity at healthy levels.12

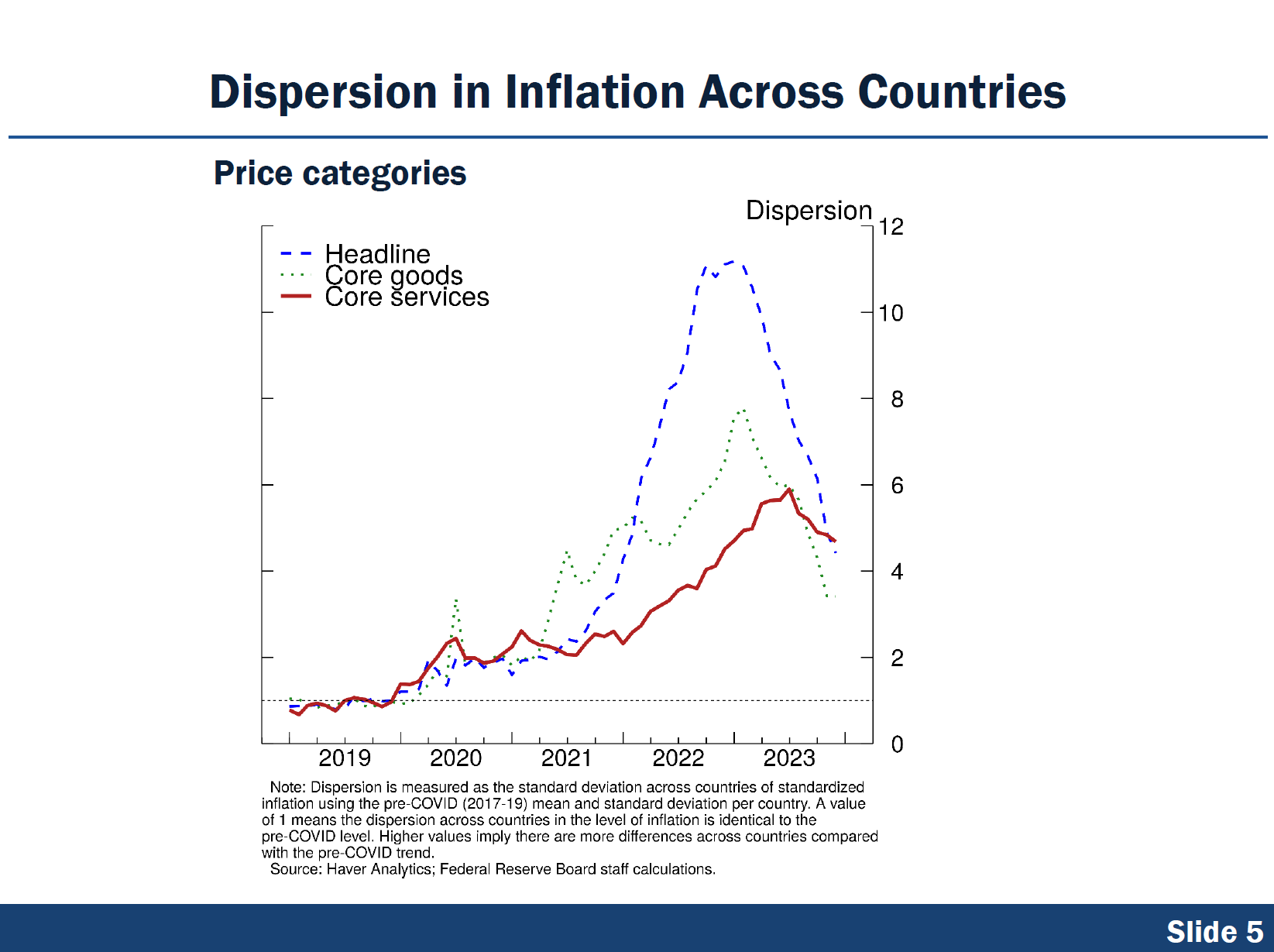

Researchers at the Board of Governors also find that differences in the pace of disinflation across countries have been largely driven by different trajectories of services price inflation.13 As shown on slide 5, they find that the dispersion of inflation across countries peaked in 2023 and has been declining since then for headline and core goods, but not so much for core services inflation, with housing developments helping to account for the differences in services inflation. Other cross-country research suggests that wage developments help explain services inflation dynamics.14 Indeed, services inflation from both the United States and the euro area have been elevated. Still, while U.S. housing services inflation has been running higher than the wage-driven nonhousing component, the reverse is true in the euro area.

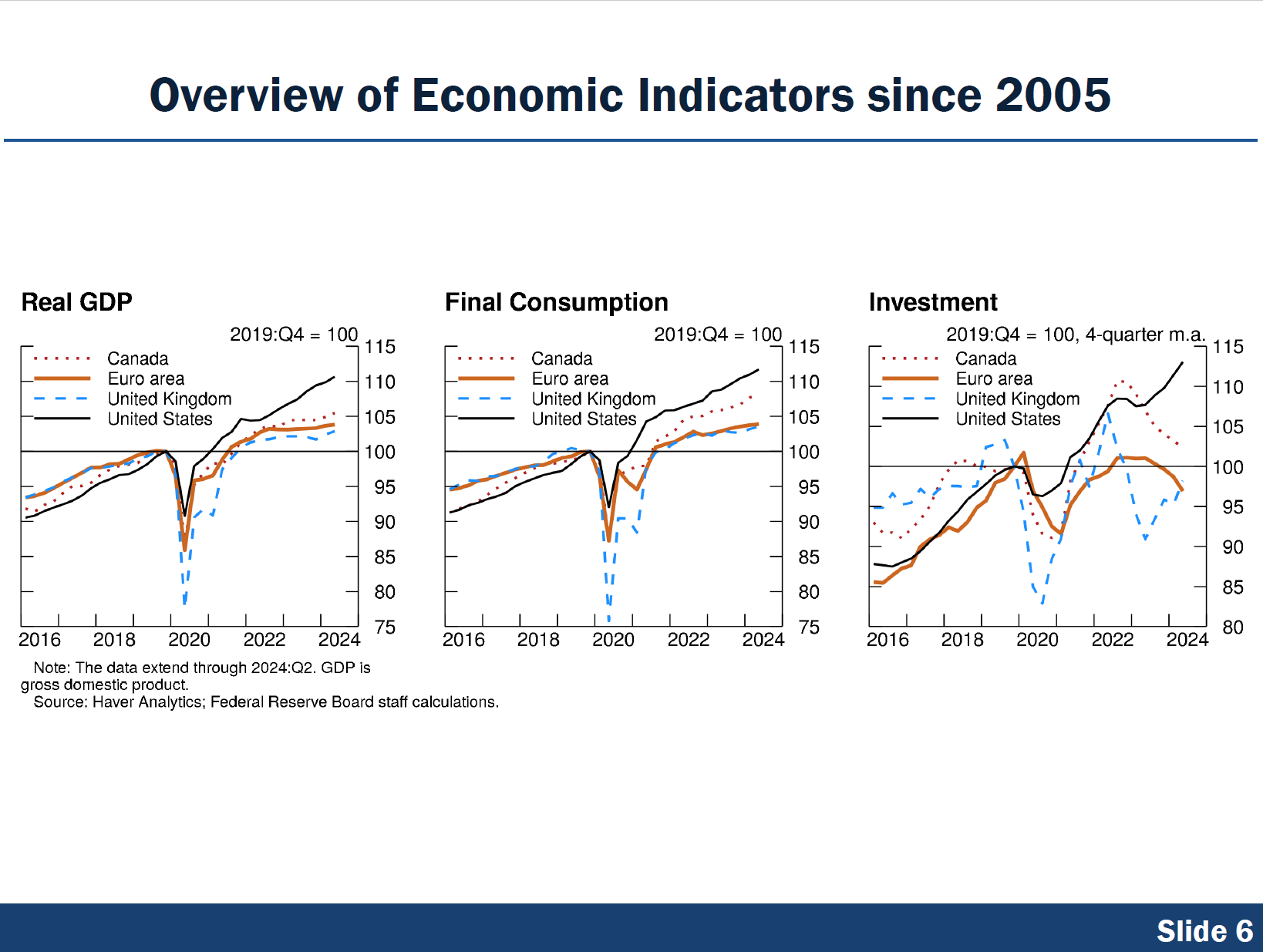

While the cross-country differences during the recent bout of high inflation have emerged more prominently during the disinflationary period, economic growth has been very heterogenous since the onset of the COVID-19 pandemic. Generally speaking, the U.S. has experienced a significantly stronger recovery than other advanced economies. As we can see in the left panel on slide 6, real GDP has grown substantially more in the United States since 2021. This is also the case with respect to the larger components of GDP, such as consumption and investment, shown in the right two panels.

In explaining why the U.S. has managed to bring down inflation and experience strong economic activity, I believe that the combination of restrictive monetary policy together with convex supply curves can help explain these developments.15 In addition, there are three supply-related factors that have also made significant contributions to the combination of rapid disinflation together with continued and resilient growth.

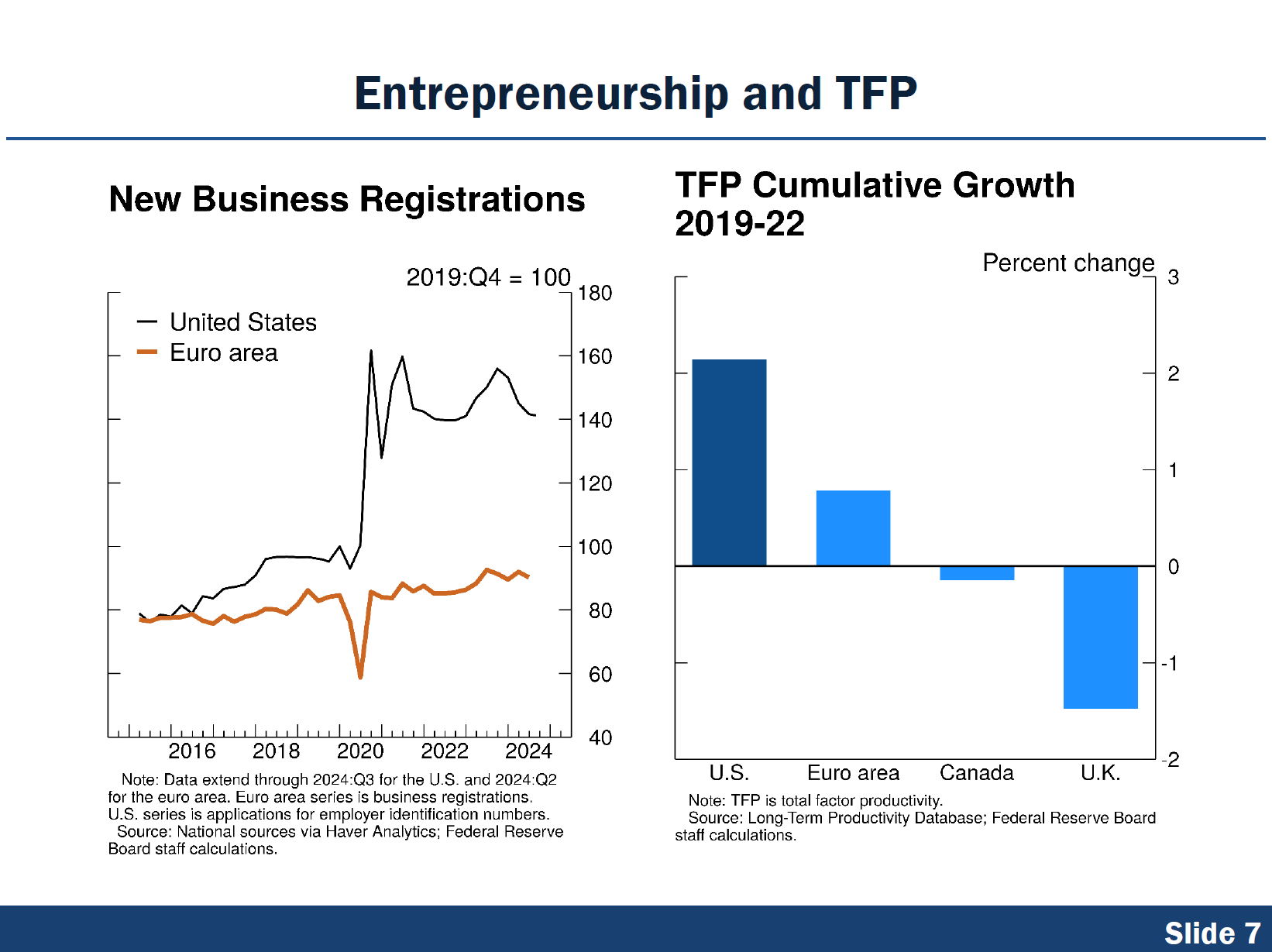

First, there are important factors that have affected total factor productivity differently across countries. For instance, the U.S. has seen greater business dynamism, as reflected in a higher rate of new business formation, shown in the left panel on slide 7. This is important because while most new firms fail, a small share of those that survive grow rapidly and make significant contributions to aggregate productivity.16 Moreover, the pandemic-era business creation surge has been particularly strong in high-tech sectors, such as computer systems design as well as research and development services.17 In fact, we have also seen greater growth in total factor productivity in the U.S. relative to other advanced economies, as shown in the right figure on slide 7. In addition, while the artificial intelligence (AI) technology is still in its nascency, U.S. businesses across different sectors of the economy are investing in and adopting AI. According to the Business Trends and Outlook Survey of the Census, more than 20 percent of companies in 15 sectors have adopted AI.18 It may be too early to tell, but additional productivity gains may be coming from tasks that are enhanced by AI through process improvements.19

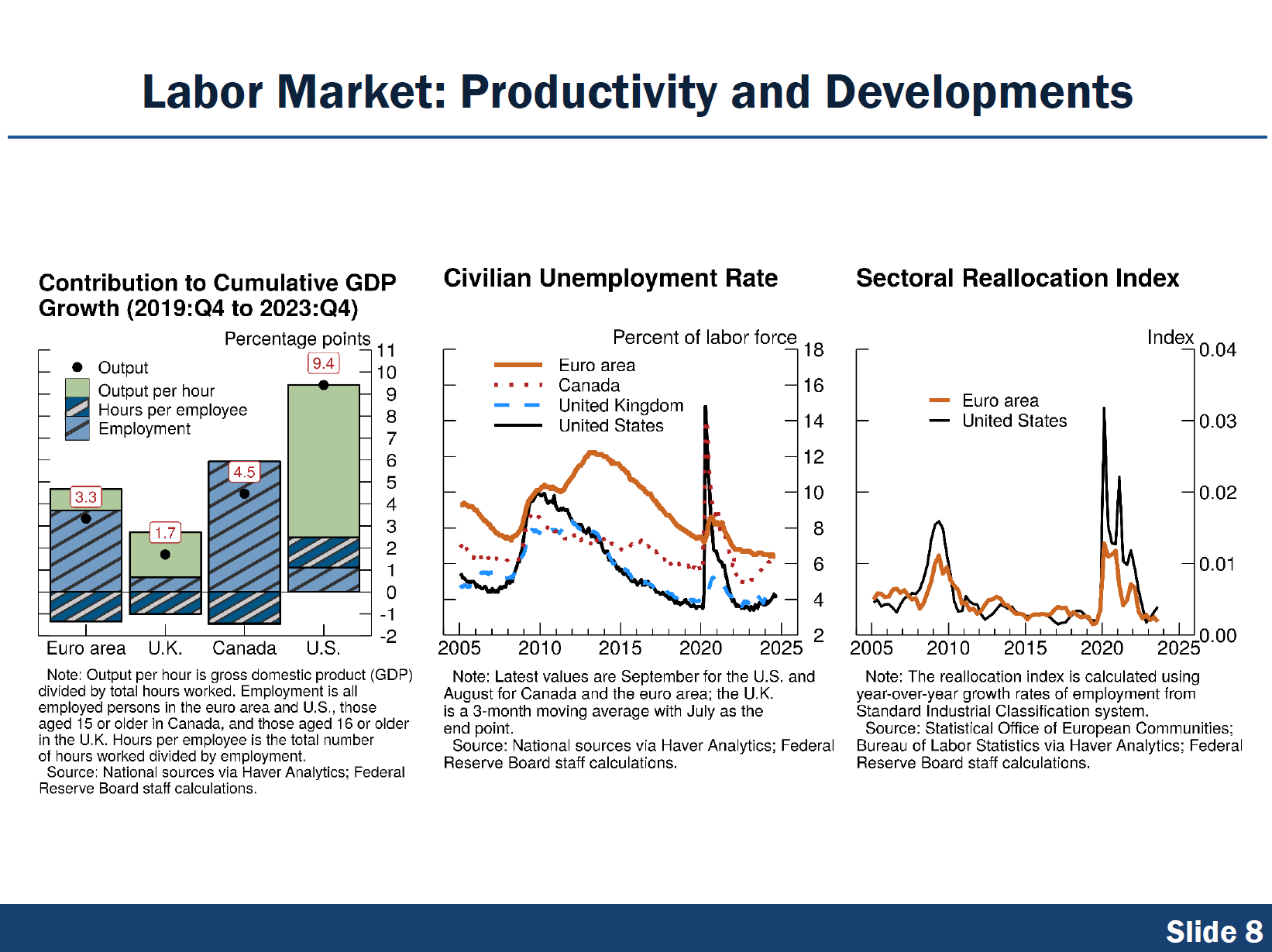

Second, we have seen a stronger rate of labor productivity growth in the United States as shown in the left panel on slide 8.20 The economic policy response to the pandemic in the U.S. was robust, but it was different from the response in many other advanced economies. In other economies, the emphasis was on maintaining employment, and specifically keeping workers employed in their existing firms when the pandemic arrived. This was the case, for example, in the euro area, and the middle panel indeed shows that the unemployment rate peaked several times higher in the United States. This approach minimized euro-area job losses, but it may have limited the flow of workers to more-productive sectors of the economy, which is supported by Federal Reserve Board research showing substantially more sectoral re-allocation of workers in the United States compared to the euro area, as seen in the right figure on slide 8.21

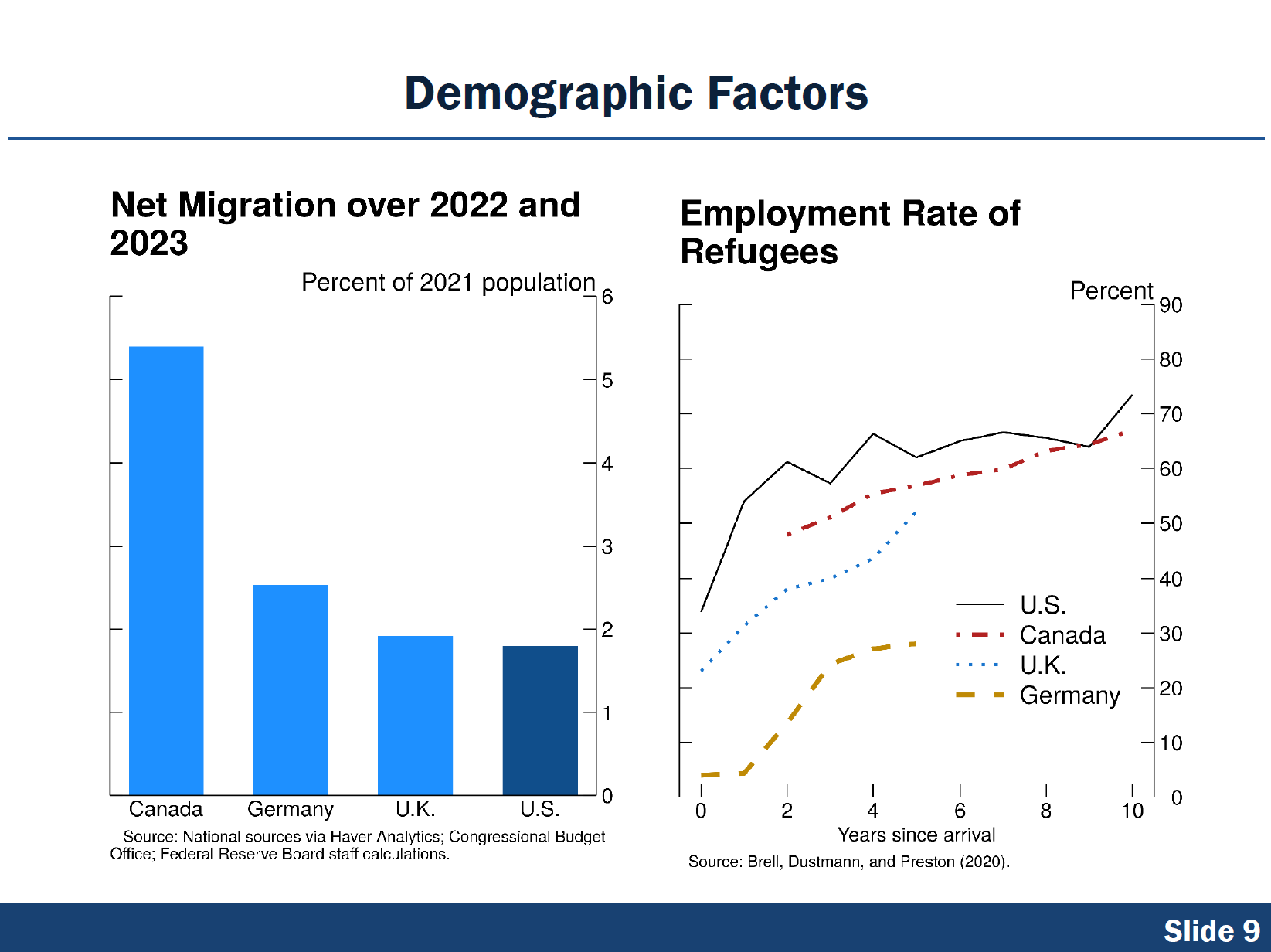

Third, the U.S. labor supply has grown in the post-pandemic period. The labor force participation rate increased solidly, especially from the beginning of 2021 through the middle of 2023, and the U.S. population increased strongly because of high levels of immigration. While recent immigration flows into some European countries have been comparable in proportion to those into the U.S., as seen in the left figure on slide 9, new immigrants may have contributed relatively more to U.S. growth because they often integrate more quickly into the labor force, as seen in the right figure.22

Finally, and turning our focus to monetary policy, this stronger economic performance, with falling inflation, has allowed the FOMC to be patient about the timing in reducing our policy rate. This performance gave us time to strongly focus on the inflation side of our mandate. And this, together with the bump in inflation early this year, helps explain why we began to ease monetary policy to less-restrictive levels only after other central banks of advanced economies had done so. But now, the combination of significant ongoing progress in reducing inflation and a cooling in the labor market means that the time has come to begin easing monetary policy, and I strongly supported the decision by the FOMC in our September meeting to cut the federal funds rate by 50 basis points.

Looking ahead, while I believe the focus should remain on continuing to bring inflation to 2 percent, I support shifting attention to the maximum-employment side of the FOMC’s dual mandate as well. The labor market remains resilient, but I support a balanced approach to the FOMC’s dual mandate so we can continue making progress on inflation while avoiding an undesirable slowdown in employment growth and economic expansion. If progress on inflation continues as I expect, I will support additional cuts in the federal funds rate to move toward a more neutral policy stance over time.

Still, my approach to any policy decision will continue to be data dependent and to rely on multiple and diverse sources of data to form my view of how the economy is evolving. For instance, I am closely monitoring the economic effects from Hurricane Helene and from geopolitical events in the Middle East, since these could affect the U.S. economic outlook. If downside risks to employment escalate, it may be appropriate to move policy more quickly to a neutral stance. Alternatively, if incoming data do not provide confidence that inflation is moving sustainably toward 2 percent, it may be appropriate to slow normalization in the policy rate.

As I have described, the escalation of inflation unleashed by the pandemic was global in scope, and the fight to reduce inflation has also been global. Each of our economies faces its own unique mixture of challenges, but by comparing our similarities and contrasting our differences, I believe we can learn from each other’s experiences.

In conclusion, let me thank those of you in this room who contribute to bridging science and practice. For those working on the policy side, thank you for the hard work you do each day to analyze the economic data that allows not only policymakers like me, but also consumers and businesses to gain a better understanding of ongoing developments in the global economy. On the academic side, thank you for your creativity and ingenuity in asking policy-relevant questions and pushing the boundaries of our understanding of an ever-changing economic landscape.

1. The views expressed here are my own and are not necessarily those of my colleagues on the Federal Reserve Board or the Federal Open Market Committee. Return to text

2. See Danilo Cascaldi-Garcia, Luca Guerrieri, Matteo Iacoviello, and Michele Modugno (2024), „Lessons from the Co-Movement of Inflation around the World,” FEDS Notes (Washington: Board of Governors of the Federal Reserve System, June 28). Return to text

3. I refer to updated estimates from the following works: Hie Joo Ahn and Matteo Luciani (2020), „Common and Idiosyncratic Inflation,” Finance and Economics Discussion Series 2020-024 (Washington: Board of Governors of the Federal Reserve System, March; revised August 2024); and Eli Nir, Flora Haberkorn, and Danilo Cascaldi-Garcia (2021), „International Measures of Common Inflation,” FEDS Notes (Washington: Board of Governors of the Federal Reserve System, November 5). Return to text

4. See Danilo Cascaldi-Garcia, Musa Orak, and Zina Saijid (2023), „Drivers of Post-Pandemic Inflation in Selected Advanced Economies and Implications for the Outlook,” FEDS Notes (Washington: Board of Governors of the Federal Reserve System, January 13). Return to text

5. See Gianluca Benigno, Julian di Giovanni, Jan J.J. Groen, and Adam I. Noble (2022), „The GSCPI: A New Barometer of Global Supply Chain Pressures,” Staff Reports 1017 (New York: Federal Reserve Bank of New York, May). Return to text

6. See Francesco Ferrante, Sebastian Graves, and Matteo Iacoviello (2023), „The Inflationary Effects of Sectoral Reallocation,” Journal of Monetary Economics, vol. 140, supplement (November), pp. S64–S81. Return to text

7. See Paul Ho, Pierre-Daniel Sarte, and Felipe Schwartzman (2022), „Multilateral Comovement in a New Keynesian World: A Little Trade Goes a Long Way (PDF),” Working Paper Series 22-10 (Richmond: Federal Reserve Bank of Richmond, November). Return to text

8. For the 1972–78 period, we define the inflation ascent path as 1972:Q3 to 1974:Q4, while its descent path is 1975:Q1 to 1978:Q2. For the 1978–86 period, we define the inflation ascent path as 1978:Q3 to 1980:Q2, while its descent path is 1980:Q3 to 1986:Q2. For the 2020–24 period, we define the inflation ascent path as 2021:Q1 to 2022:Q4, while its descent path is 2023:Q1 to 2024:Q1 because it is the latest available data. Return to text

9. See Domenico Giannone and Giorgio Primiceri (2024), „The Drivers of Post-Pandemic Inflation,” NBER Working Paper Series 32859 (Cambridge, Mass.: National Bureau of Economic Research, August). Return to text

10. For the economic effects on the size of fiscal stimuli, see Oscar Jorda and Fernanda Nechio (2023), „Inflation and Wage Growth since the Pandemic,” European Economic Review, vol. 156, 104474. Return to text

11. See Christiane Baumeister, Gert Peersman, and Ine Van Robays (2010), „The Economic Consequences of Oil Shocks: Differences across Countries and Time (PDF),” in Renee Fry, Callum Jones, and Christopher Kent, eds., Inflation in an Era of Relative Price Shocks (Sydney: Reserve Bank of Australia), pp. 91–128; and Andrea De Michelis, Thiago Ferreira, and Matteo Iacoviello (2020), „Oil Prices and Consumption across Countries and U.S. States,” International Journal of Central Banking, vol. 16 (March), pp. 3–43. Return to text

12. For the effects of labor market tightness on price and wage inflation, see Olivier J. Blanchard and Ben S. Bernanke (2022), „What Caused the U.S. Pandemic-Era Inflation?” NBER Working Paper Series 31417 (Cambridge, Mass.: National Bureau of Economic Research, June); Olivier J. Blanchard and Ben S. Bernanke (2024), „An Analysis of Pandemic-Era Inflation in 11 Economies,” NBER Working Paper Series 32532 (Cambridge, Mass.: National Bureau of Economic Research, May). Return to text

13. See Maria Aristizabal-Ramirez, Dylan Moore, and Eva Van Leemput (forthcoming), „What Goes Up Together Must Not Come Down Together: An Analysis of Services Disinflation,” Forthcoming as an International Finance Discussion Paper (Washington: Board of Governors of the Federal Reserve System). Return to text

14. See Pongpitch Amatyakul, Deniz Igan, and Marco Jacopo Lombardi (2024), „Sectoral Price Dynamics in the Last Mile of Post-COVID-19 Disinflation,” BIS Quarterly Review, March, pp. 45–57. Return to text

15. See Adriana D. Kugler (2024), „Disinflation without a Rise in Unemployment? What Is Different This Time Around,” speech delivered at the 2024 Stanford Institute for Economic Policy Research Economic Summit, Stanford University, Stanford, Calif., March 1. Return to text

16. See Titan Alon, David Berger, Robert Dent, and Benjamin Pugsley (2018), „Older and Slower: The Startup Deficit’s Lasting Effects on Aggregate Productivity Growth,” Journal of Monetary Economics, vol. 93 (January), pp. 68–85; and Ryan Decker, John Haltiwanger, Ron Jarmin, and Javier Miranda (2014), „The Role of Entrepreneurship in U.S. Job Creation and Economic Dynamism,” Journal of Economic Perspectives, vol. 28 (Summer), pp. 3–24. Return to text

17. See Ryan Decker and John Haltiwanger (2024), „High Tech Business Entry in the Pandemic Era,” FEDS Notes (Washington: Board of Governors of the Federal Reserve System, April 19). Return to text

18. In data released September 23, 2024, the share of firms reporting the use of AI to perform tasks previously done by employees in producing goods or services was 27 percent. Return to text

19. See Lisa D. Cook (2024), „Artificial Intelligence, Big Data, and the Path Ahead for Productivity,” speech delivered at „Technology-Enabled Disruption: Implications of AI, Big Data, and Remote Work,” a conference organized by the Federal Reserve Banks of Atlanta, Boston, and Richmond, Atlanta, October 1. Return to text

20. See Francois de Soyres, Joaquin Garcia-Cabo Herrero, Nils Goernemann, Sharon Jeon, Grace Lofstrom, and Dylan Moore (2024), „Why Is the U.S. GDP Recovering Faster than Other Advanced Economies?” FEDS Notes (Washington: Board of Governors of the Federal Reserve System, May 17). Return to text

21. See Joaquin García-Cabo, Anna Lipińska, and Gaston Navarro (2023), „Sectoral Shocks, Reallocation, and Labor Market Policies,” European Economic Review, vol. 156 (July), 104494. Return to text

22. See Courtney Brell, Christian Dustmann, and Ian Preston (2020), „The Labor Market Integration of Refugee Migrants in High-Income Countries,” Journal of Economic Perspectives, vol. 34 (Winter), pp. 94–121. Return to text

https://www.federalreserve.gov/newsevents/speech/kugler20241008a.htm

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

COMMENTS